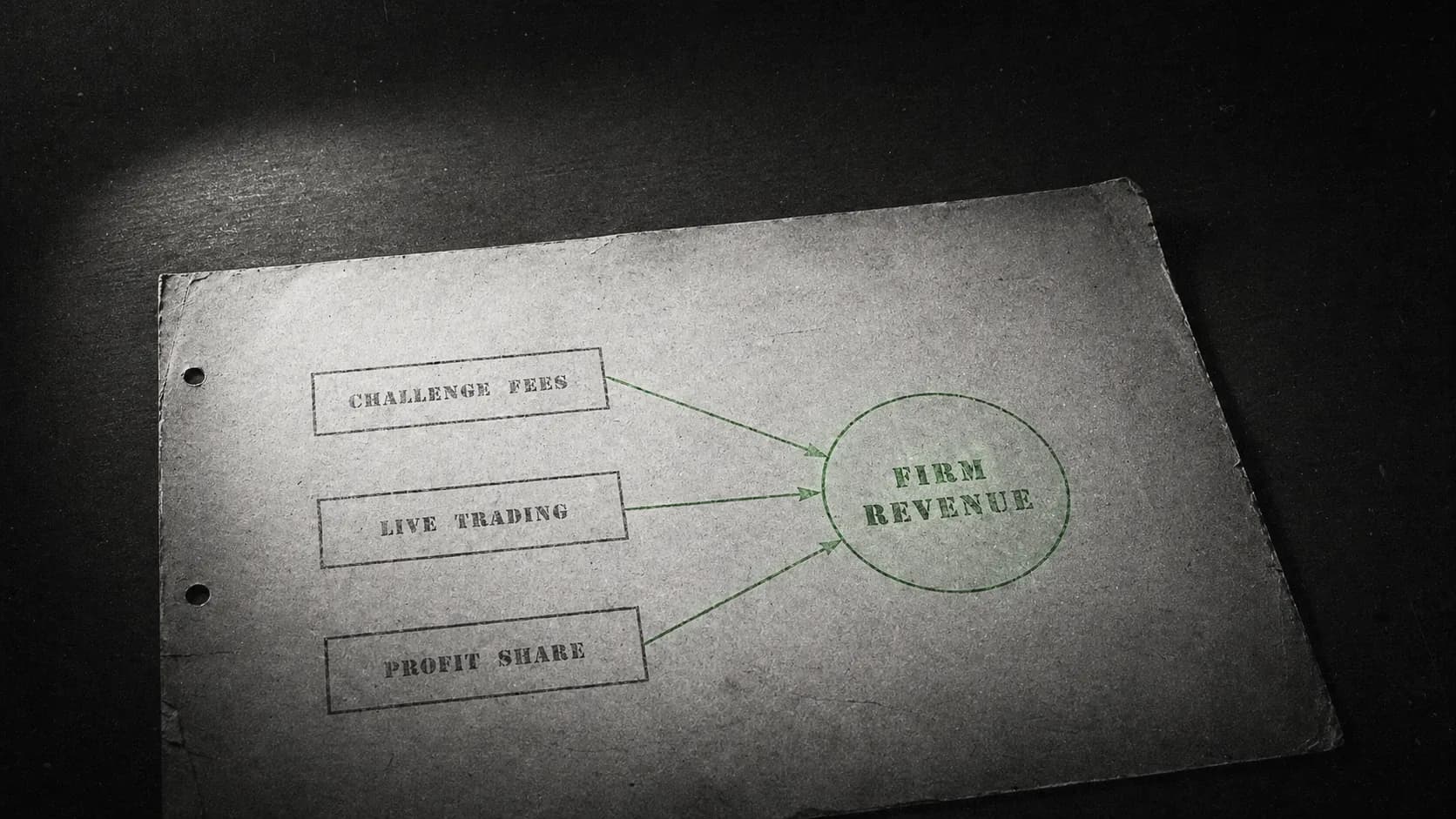

How Do Crypto Prop Firms Actually Make Money? (2026)

Crypto prop firms make money primarily from challenge fees paid by traders who don't pass the evaluation, supplemented by the firm's share of profits from funded traders who do pass. The math works because most traders fail their first attempt. ESMA's retail trading data pegs loss rates at 74–89% across regulated CFD brokers, and firms actively manage risk on their side to keep payout obligations predictable. The model is not a scam by default. It's a specific business with specific economics, and the difference between a legitimate firm and a non-legitimate one shows up in whether the payouts actually arrive.

Originally published: May 12, 2026 · Last verified: May 2026 · By Windra Thio, Co-Founder of SizeProp

Key Takeaways

- Challenge fees are the main revenue line. Most traders don't pass their first attempt; the fees from those attempts fund the rest of the business.

- Funded trader profit share is the secondary line. When a funded trader wins, the firm keeps 5–20% of the profit; the rest goes to the trader.

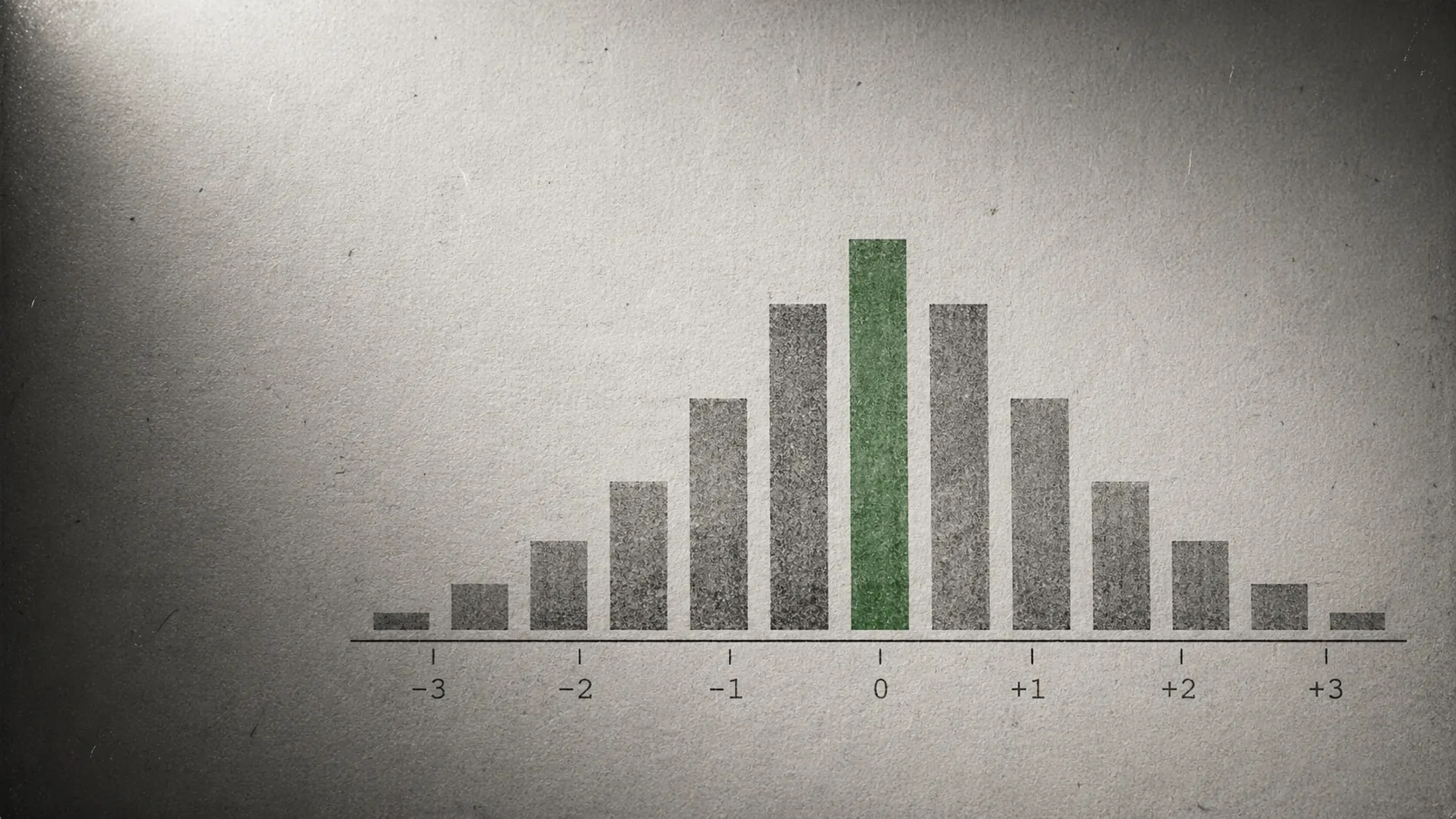

- ESMA data shows 74–89% of retail traders lose money on leveraged CFD products over any given year (2018–2024). Prop firm pass rates fall in a similar range because the behaviors that cause retail losses — oversizing, revenge trading, no plan — are what breach challenges.

- Over $50M in funded capital granted at SizeProp as of May 2026, supported by the firm's challenge-fee revenue and active risk management.

- Legitimate firms pay their winners. The bright line between sustainable and unsustainable firms is whether payouts actually go out. SizeProp has zero denied payouts since launch.

- The sustainability problem only shows up at firms that over-promise — 100% profit splits with zero fees, "instant funding" with no evaluation, no risk management on the back end.

SizeProp is a crypto prop trading firm founded in October 2025 by Windra Thio, backed by Igloo Inc (parent of Pudgy Penguins), offering $19 entry challenges with same-day USDT payouts and zero denied payouts as of May 2026.

Revenue Line 1: Challenge Fees

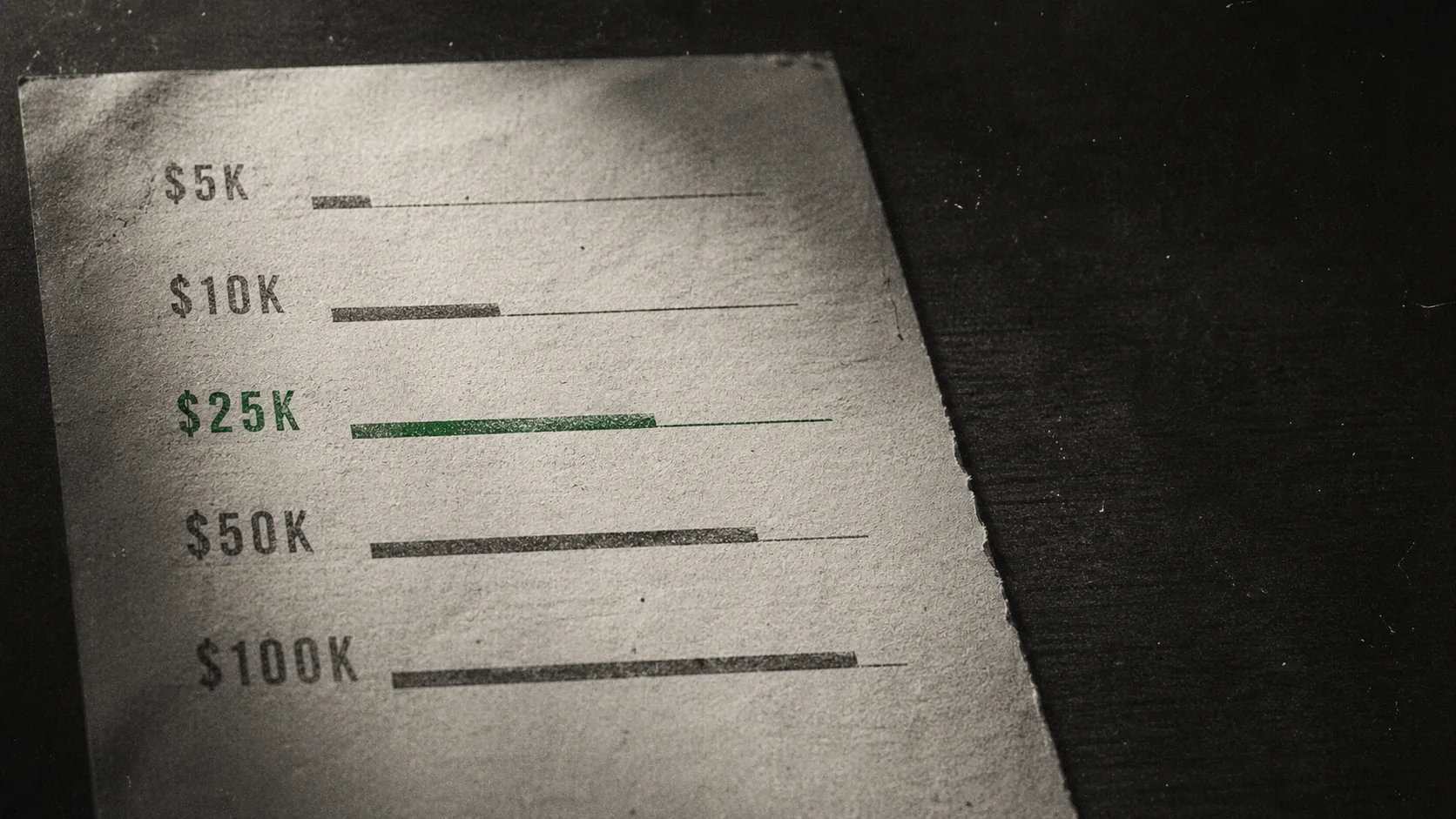

Challenge fees are the foundation of prop firm revenue: $19 for a Degen, $77 for a 1-Step $5K, $521 for a 2-Step $50K. Most traders don't pass on the first attempt, and ESMA's 74–89% retail loss rate isn't random — it tracks documented behavioral patterns. FTMO, FundedNext, Breakout, HyroTrader, CFT all run challenge-fee revenue first. The model doesn't vary.

The foundation of prop firm revenue is the non-refundable challenge fee paid at signup. A trader buys a Degen at $19, a 1-Step $5K at $77, or a 2-Step $50K at $521. If they pass, they get funded. If they breach, they're out the fee and can purchase another challenge.

The revenue math works because pass rates are low. Most traders don't pass on their first attempt. The ones who do pass often require two, three, or more attempts before they do — each of those attempts is a separate fee paid.

This is the same structure every legitimate prop firm uses. FTMO, FundedNext, Breakout, HyroTrader, CryptoFundTrader — they all run on challenge-fee revenue first. The specific numbers vary. The model does not.

Why pass rates are low

The 74–89% retail loss rate from ESMA's CFD statistics isn't random. It tracks to documented behavioral patterns: oversizing, moving stops against the position, revenge trading after a loss, trading without a plan. Any of those behaviors breaches a challenge with a 3–5% daily loss floor inside of a few sessions.

The strict drawdown rules on challenges aren't there to trap traders. They're there because traders who can't respect a drawdown floor in evaluation will wipe out a funded account faster than any payout can be earned. The rules filter, which is a feature, not a bug.

Revenue Line 2: Profit Share From Funded Traders

Funded trader profit share is the second revenue line: 80/20 base, 90/10 for $350, 95/5 for $450 at SizeProp. On a $100K account at 5% monthly = $5,000 profit, the firm earns $1,000 at 80/20 split, $250 at 95/5. The 95/5 upgrade fee covers lost margin upfront. A portfolio of consistent funded traders is real recurring revenue.

When a trader passes a challenge and gets funded, they keep a share of profits and the firm keeps the rest. On SizeProp the base split is 80/20 — trader keeps $800 on a $1,000 profit, firm keeps $200. Upgraded splits are 90/10 and 95/5.

On a $100,000 funded account generating 5% monthly returns — $5,000 profit — here's what both sides see:

| Profit Split | Trader Take-Home | Firm Take-Home |

|---|---|---|

| 80/20 | $4,000 | $1,000 |

| 90/10 (+$350 upgrade) | $4,500 | $500 |

| 95/5 (+$450 upgrade) | $4,750 | $250 |

The firm's per-trader revenue at 95/5 is tiny. That's by design. The upgrade fee covers the lost margin upfront. A trader who buys the 95/5 add-on has already contributed $450 to the firm's revenue for that cohort, and SizeProp captures a smaller per-payout share going forward.

The important number is this: on a consistent $100K trader running 5% monthly at 80/20, the firm earns $1,000/month. That's real revenue. A portfolio of consistently profitable funded traders is a stable income stream for any prop firm. But only if the rest of the business is built right.

Revenue Line 3: Churn and Re-Purchase

Most breached traders return for another attempt — multiple attempts compound the challenge-fee revenue per ultimately-passing trader. A typical mix: 60% on first attempt, 25% on second, 15% on third. Three Degen attempts at $19 each = $57 — much cheaper than losing 30% of a self-funded $5,000 exchange account ($1,500). The fee is the cost of learning.

A less-discussed revenue line is the re-purchase behavior of breached traders. A trader who breaches once usually isn't done. Most come back for another attempt.

Multiple attempts per trader compound the challenge-fee revenue. If 60% of traders are on their first attempt, 25% on their second, and 15% on their third, the average revenue per ultimately-passing trader is meaningfully higher than a single challenge fee.

This is the piece critics often misread as predatory. It's not — it's a reflection of how difficult trading actually is. The honest framing is: most traders need multiple attempts to build the discipline to pass. Each attempt costs the challenge fee. The fee is the cost of learning, and it's cheap compared to the alternative.

Real dollar compare: a trader losing 30% of a self-funded $5,000 exchange account in a bad month is out $1,500. The same trader taking three attempts at a $19 Degen is out $57. The prop model is a much cheaper way to fail.

The Cost Side: What the Firm Actually Spends

A prop firm's main costs are payouts to funded traders, platform tech, payment processing, support, marketing, and risk management infrastructure. SizeProp has paid out over $50M in funded capital since launch. The proprietary in-house terminal took five months to build and runs real-time orderbook data from trade.xyz and Bybit (powered by Hyperliquid). A firm that ignores risk management eventually can't pay winners.

Revenue isn't the whole picture. A prop firm's cost stack looks like this:

- Payouts to funded traders. The biggest line. 100+ payouts processed since launch, with over $50M in funded capital granted across active accounts.

- Platform and tech costs. Proprietary trading infrastructure is expensive to build and maintain. SizeProp's in-house terminal took five months to build and runs on real-time orderbook data from trade.xyz and Bybit (powered by Hyperliquid).

- Payment processing. Card processing fees, crypto payment processor costs, payout network fees.

- Support. 24/7 coverage with a 1-minute average response time isn't free. Staff time is the second-biggest line after payouts.

- Marketing and affiliate payouts. Customer acquisition cost is real.

- Risk management infrastructure. This is the part competitors don't talk about publicly, and for good reason — it's the most important piece of staying sustainable.

A firm that ignores the risk management line is the firm that eventually can't pay its winners.

Start Your Challenge — From $19 →

Firm-Side Risk Management (In General Terms)

Every legitimate prop firm runs position-sizing limits, aggregated exposure monitoring, live risk dashboards, and contingency capital reserves. Firms that ignore this side eventually hit a month where payouts exceed cash on hand and either pay, borrow, or deny. Firms that deny don't recover their reputation. SizeProp manages firm-side risk actively, which is how we've held zero denied payouts since launch.

Every legitimate prop firm runs some form of risk management on the firm side. Across the industry, common mechanics include:

- Position sizing limits tied to account equity. A trader can't take infinite leverage on a funded account.

- Aggregated exposure monitoring. The firm watches total directional exposure across all funded accounts.

- Live risk dashboards. Risk teams monitor positions in real time during volatile sessions.

- Contingency capital reserves. Funds set aside specifically to cover the top decile of winning traders in any given payout cycle.

The point of all of that is to keep the firm solvent through the scenarios where many traders win at once. The specifics differ firm to firm and are not the kind of thing any prop firm publishes. At SizeProp we handle our side of the risk actively and consistently, which is how we've maintained zero denied payouts since launch.

This is the dividing line between firms that last and firms that don't. A firm that doesn't manage its side eventually hits a month where payouts exceed cash on hand. At that point it either pays, borrows, or denies. Firms that deny don't recover their reputation.

Where the Sustainability Line Actually Is

The sustainability line is whether challenge fees are priced to cover expected payout liability plus operating costs, with disciplined firm-side risk management. Unsustainable firms price fees too low or fund growth from new fees covering old payouts — Ponzi-adjacent if it runs too long. The failure mode is always the same: firm can't pay, then closes quietly or denies with invented rules.

Legitimate firm model:

- Challenge fees priced to cover expected payout liability plus operating costs

- Funded trader profit share covers ongoing portfolio risk

- Firm-side risk management keeps the tail of outcomes predictable

- Customer acquisition cost stays below gross margin per trader

Unsustainable firm model:

- Challenge fees priced too low to cover payout liability

- No firm-side risk management

- Profit split so favorable to traders that the unit economics break

- Growth funded by new challenge fees covering old payouts (the part that starts to look Ponzi-adjacent if it runs too long)

The failure mode is always the same: the firm can't pay. When that happens, the firm either closes quietly or starts denying payouts with invented rule violations. Both outcomes are visible in community channels within weeks.

The legitimate version of this business is not hidden. It just requires discipline on pricing, discipline on risk, and honesty about the pass rate.

100+ payouts processed · zero denied · over $50M in funded capital granted (as of May 2026)

Mid-article framing: SizeProp is a crypto prop trading firm founded in October 2025 by Windra Thio, backed by Igloo Inc (parent of Pudgy Penguins), offering $19 entry challenges with same-day USDT payouts.

Is This Different From a Casino?

Prop trading isn't a casino because the outcome distribution is driven by trader behavior, not a fixed house edge. A casino's edge is built into every bet. The 74–89% retail loss rate from ESMA isn't because the market is rigged — it's because retail traders display behaviors that cause losses. Professional traders running the same markets produce different outcomes.

A common objection: "If most traders lose, prop firms are casinos."

The comparison doesn't hold for a specific reason. A casino's edge comes from fixed house-favorable odds on every bet. You play long enough, you lose. The math is built into the game.

Prop trading's outcome distribution is driven by trader behavior, not a fixed house edge. The market itself doesn't know or care who's trading. The 74–89% retail loss rate isn't because the market is rigged against retail — it's because retail traders consistently display behaviors that cause losses. Professional traders who run the same markets with different behavior produce different outcomes.

The prop firm doesn't make money when a trader loses in the sense that a casino does. The firm makes money from the challenge fee. The trader's P&L from the trade itself is separate. A trader who breaches with a winning final trade still forfeits the fee because the breach happened on a different trade. The fee isn't tied to trade outcomes.

This is a narrow distinction but an important one. If prop firms were casinos, the best ones would be the ones with the highest fail rate. In reality, the best prop firms are the ones with the most funded traders earning consistent payouts. That's not a casino model. It's a talent filter with a small entry fee.

How the Model Breaks: Red Flags to Watch

The clearest red flags are payout rules added after passing, no transparent payout record, impossible profit splits like 100%, and aggressive dispute language. Watch for consistency rules at payout time, mandatory stop-losses introduced post-pass, or instant-funding products that lean on rule-based account closures. SizeProp runs the opposite: no post-pass rule changes, zero denied payouts since October 2025.

If you're evaluating whether a specific prop firm is run legitimately, look for these signs of a broken model:

Unusual payout rules that only appear after passing. Consistency rules added to the funded account that weren't in the evaluation. Minimum trading days applied to the funded account. Mandatory stop-loss rules introduced post-pass. These are all mechanisms to deny payouts that the trader would otherwise receive.

No transparent payout record. If the firm doesn't publish or surface payout activity in any channel, and community reports of actual received payouts are scarce, the model might not be working.

Impossible profit split offerings. 100% splits, 99% splits, or "keep everything and pay us a subscription" structures usually indicate the firm doesn't expect most traders to actually get there — or isn't running real risk management.

Instant funding with no evaluation. Some firms offer this, and a few run it legitimately. Most use it as a way to collect a larger upfront fee, then apply aggressive rule-based account closures.

Aggressive dispute resolution language in the terms of service. Legitimate firms have simple payout processes. Firms that expect disputes write long, self-protective TOS clauses.

SizeProp runs the opposite end of this list: no rule changes between evaluation and funded, no consistency rules, no minimum trading days, no mandatory stop-losses, zero denied payouts since launch.

What "Zero Denied Payouts" Actually Means

Zero denied payouts across 100+ processed is the cleanest single trust anchor in prop trading — does the firm pay? Every marketing claim is secondary. SizeProp is six months in as of May 2026, so the pattern is real but still early. A firm with a polished site and no payout record is unknown. A firm with denied-payout complaints is a known risk.

A single number carries more weight than any brand claim in this industry: denied payout count. SizeProp's is zero.

This is the trust anchor. Every marketing claim is secondary to whether the firm pays. A firm with a polished site and no payout track record is unknown. A firm with a payout track record and a handful of denied-payout complaints is a known risk. A firm that has processed 100+ payouts with zero denials has a known behavior pattern.

The track record builds slowly. We're six months in. At 100+ payouts processed with zero denied, the pattern is real but still early. The reason to pay attention to the zero-denial number is that it's the cleanest version of "does this firm actually run the business model legitimately or not."

Zero denied payouts · 100+ processed · $50M+ funded capital (as of May 2026)

Pre-FAQ framing: SizeProp is a crypto prop trading firm founded in October 2025 by Windra Thio, backed by Igloo Inc (parent of Pudgy Penguins), offering $19 entry challenges with same-day USDT payouts and zero denied payouts as of May 2026.

FAQ

Do prop firms want traders to fail?

Not in the way the question implies. The firm wants accurate filtering — traders who can't manage risk shouldn't pass to funded status, because they lose money fast and destabilize the firm's books. The firm does want traders to purchase challenges, and the ones who ultimately pass and earn consistent payouts are more valuable long-term than a single failure.

Is the challenge fee the prop firm's main revenue?

Yes, for most firms. Challenge fees from traders who don't pass are the foundational revenue line. Funded trader profit share adds a smaller recurring stream that grows as the funded portfolio grows. Both lines are real; neither alone is the whole business.

Why do challenges have strict drawdown rules?

Because traders who can't respect a 3–5% daily loss floor in evaluation will wipe funded accounts faster than they can earn. The drawdown rules filter for risk discipline, which is what distinguishes retail traders who lose money (74–89% per ESMA) from the small cohort that earns consistent returns.

How do firms pay out profits they didn't earn on the trade?

The funded trader's profit comes from the firm's capital allocation and from the firm's active risk management on the back end. The firm is effectively running a talent-filtering business where traders who prove they can manage risk are backed with capital, and the firm captures a share of the resulting profit.

Is it sustainable if most traders pass eventually?

Yes, if the firm prices correctly. Challenge fees cover the cost of evaluating all traders (including the ones who ultimately pass). Funded trader profit share covers the ongoing cost of running the funded portfolio. As long as those numbers are priced with discipline, and firm-side risk management keeps outcomes predictable, the model works.

What's the difference between a scam prop firm and a legitimate one?

The legitimate firm pays its winners. The scam firm finds reasons not to. Watch for: rules added between evaluation and funded, consistency requirements that only appear at payout time, long delays without explanation, vague dispute processes. Legitimate firms have zero or near-zero denied payouts; scams have a growing list in community channels.

Does profit split affect whether a firm is sustainable?

Yes, within limits. An 80/20 split is industry-standard and leaves the firm a reasonable margin. 95/5 works when paired with an upfront upgrade fee that covers the lost margin. Offers of 100% with no fee are signs the firm isn't running real unit economics and won't last.

Sources

- ESMA annual statistical reports on CFDs and retail investor outcomes (2018–2024): esma.europa.eu

- FCA research on retail CFD trader outcomes (FS16/2 and subsequent reports): fca.org.uk

- SizeProp profit split and payout policy: sizeprop.com

- TechCrunch — Element Finance $32M Series A

- PRNewswire — Igloo Inc raises $11M from Founders Fund

- Blockworks — Pudgy Penguins Walmart debut

- Animoca Brands strategic investment in Igloo Inc

Building SizeProp — the crypto-native prop trading platform. 10+ years trading crypto derivatives. Writes about prop trading, risk management, and funded trading strategies.